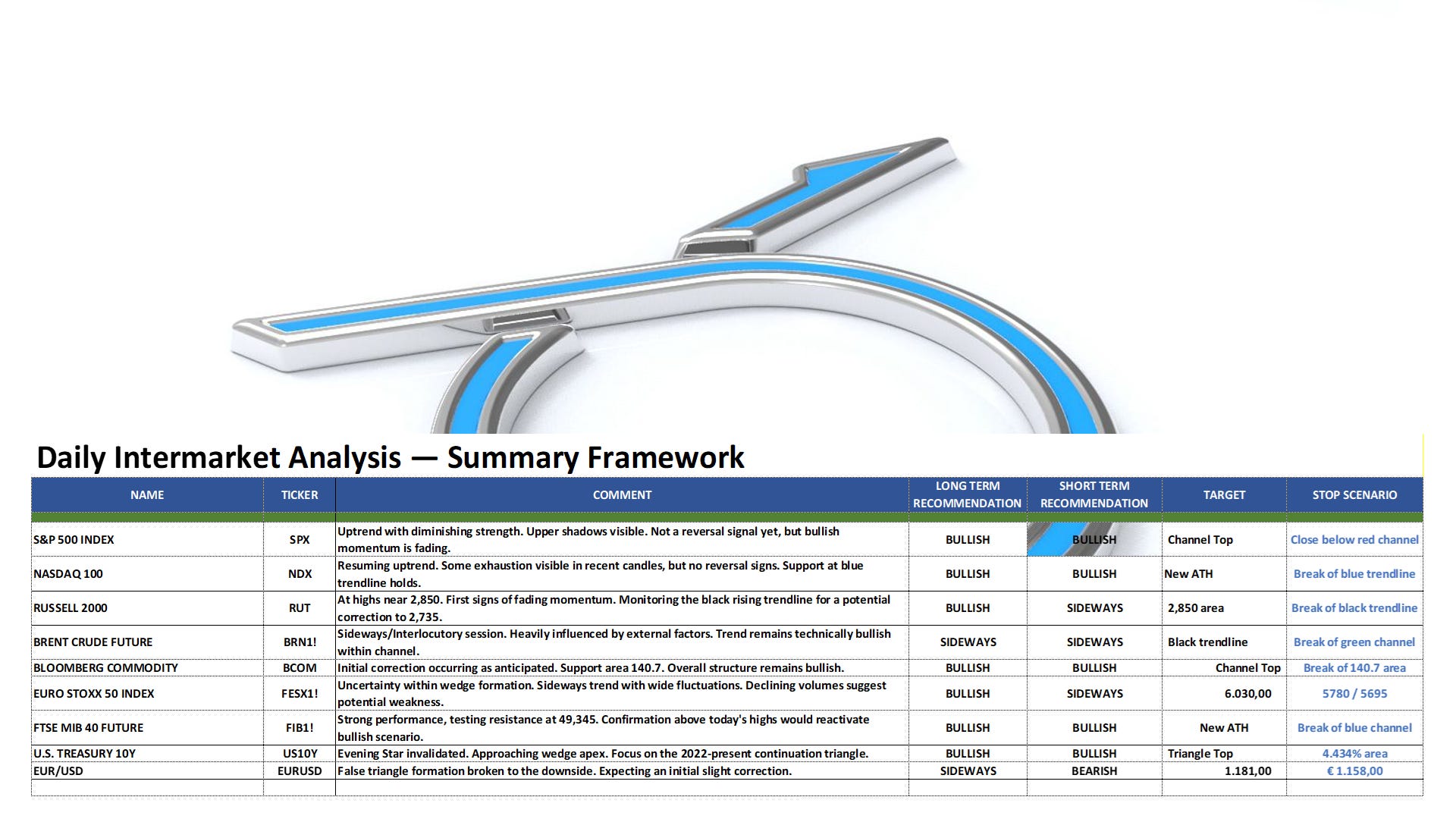

DAILY INTERMARKET ANALYSIS (15/05/2026)

S&P 500 Index, Nasdaq 100, Brent Crude Futures, Bloomberg Commodity Index, EuroStoxx 50, U.S. 10‑Year Treasury Yield, Euro / U.S. Dollar, RUSSELL 2000

SPX – S&P 500 Index

SPX S&P 500: The candlestick analysis of the recent sessions shows a U.S. Index in an uptrend, but with diminishing strength. Although the trend remains upwardly biased and shows no signs of reversal, the candles from the last few trading days exhibit rather pronounced upper shadows (wicks). We confirm that this is not a reversal signal, but it clearly indicates that bullish momentum is fading. Therefore, we remain Bullish and maintain the red rising channel on the chart as the stop level for our scenario.

NDX – Nasdaq‑100 Index

NDX: The Nasdaq 100 is resuming the uptrend we have been following. Similar to the S&P 500, we notice some exhaustion in the bullish thrust within the candles of the last few days. However, these are not reversal signals; therefore, we remain Bullish, maintaining the blue rising trendline on our chart as the stop level for our scenario.

BRN1! – Brent Crude Futures

BRN1!: Another sideways session that confirms how the future is heavily influenced by external factors. Technically, the trend remains bullish and continues to hold within our channel. The black trendline may act as a resistance level

BCOM – Bloomberg Commodity Index

BCOM: As anticipated yesterday, we have seen an initial correction that could find support in the 140.7 area. We maintain our Bullish outlook. Any downward break of the aforementioned support could project the Index toward the lower boundary of the red rising channel on our chart

FESX Future EURO STOXX 50 EUR

FESX1!: The trend of the European future remains highly uncertain within the wedge—a formation that is notoriously difficult to track because the price action inside these patterns is typically sideways, characterized by wide fluctuations with higher highs and lower lows. Therefore, we are not changing our outlook, which remains sideways. Trading volumes in recent sessions have been declining, which could weaken the trend in the coming days.

FTSEMIB – FTSE MIB 40 FUTURE

FIB1! – FTSE MIB 40 FUTURE: A great show of strength. The Italian future stopped just 20 points shy of the all-time high recorded on May 7th, thus moving above the resistance level we previously identified at 49,345. Should tomorrow's session close above today's highs, it would reactivate our Bullish scenario. In that case, we would use either this level or the base of the blue rising channel as our stop.

US10Y – U.S. Treasury Bond 10‑Year Yield

US10Y: Lack of confirmation for yesterday's candle (Evening Star). The U.S. 10-year yield continues its run, now very close to the apex of the wedge we previously highlighted. Generally, this is a bearish pattern (marked in black on our chart). However, the continuation of the trend within the formation leads us to focus on the triangle in place since late 2022 (marked in red on our chart), which, by contrast, is a technical continuation pattern.

EUR/USD – Euro vs U.S. Dollar

EURUSD: The small triangle we recently drew on the chart is not, in fact, a formal technical triangle formation, despite its appearance. It lacks the four alternating points of contact on the two converging trendlines required for validation. Nevertheless, we are treating the downward breakout as a signal for an initial, slight correction.

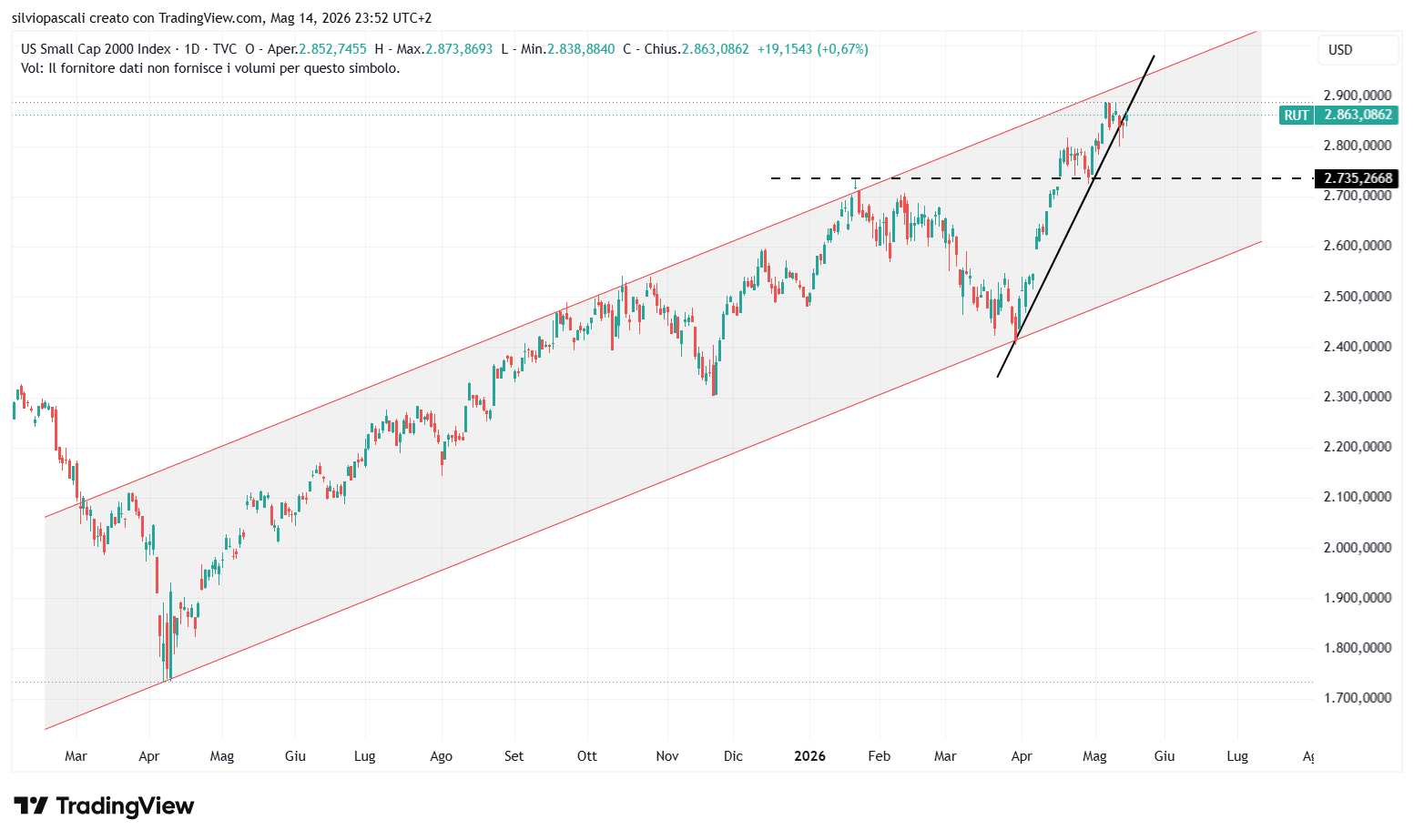

RUSSELL 2000 (Small cap Index)

RUT: We are introducing the Russell 2000 as a key indicator for U.S. small caps. The Index, currently at its highs (near the 2,850 area), is showing the first signs of fading momentum. We will monitor whether it can hold its short-term black rising trendline or if it will undergo a correction toward the support area at 2,735.

This article is for informational and educational purposes only and reflects my opinions as of the publication date. It is not investment advice, legal advice, tax advice, or a recommendation to buy or sell any security. I may hold positions in securities discussed, and my views may change without notice. Readers should do their own work and consult their own advisors before making investment decisions.